Income

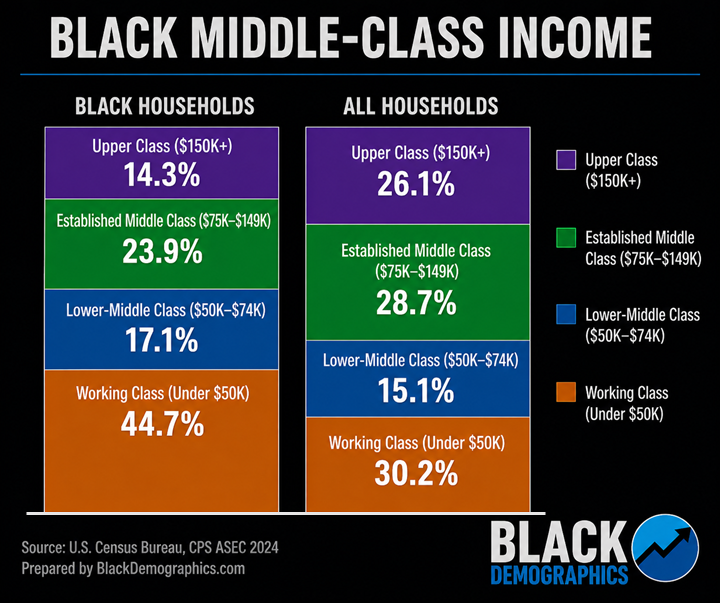

What “middle class” means:

“Middle class” and “middle class income” are related but not exactly the same. Middle class usually refers to a way of life—being able to cover basic needs, pay bills, and have some financial stability. Middle class income is a way to measure that using numbers. One common method, used by the Pew Research Center, defines middle class as households earning about two-thirds to twice the U.S. median income.

Using that idea, this chart breaks income into simple groups. Households earning $75,000 to $149,999 are called “Established Middle Class,” meaning they are more financially stable. Those earning $50,000 to $74,999 are “Lower-Middle Class.” Households below $50,000 are labeled “Working Class,” and those earning $150,000 or more are “Upper Class.” All data comes from the U.S. Census Bureau Current Population Survey (CPS ASEC 2024).

Net Worth

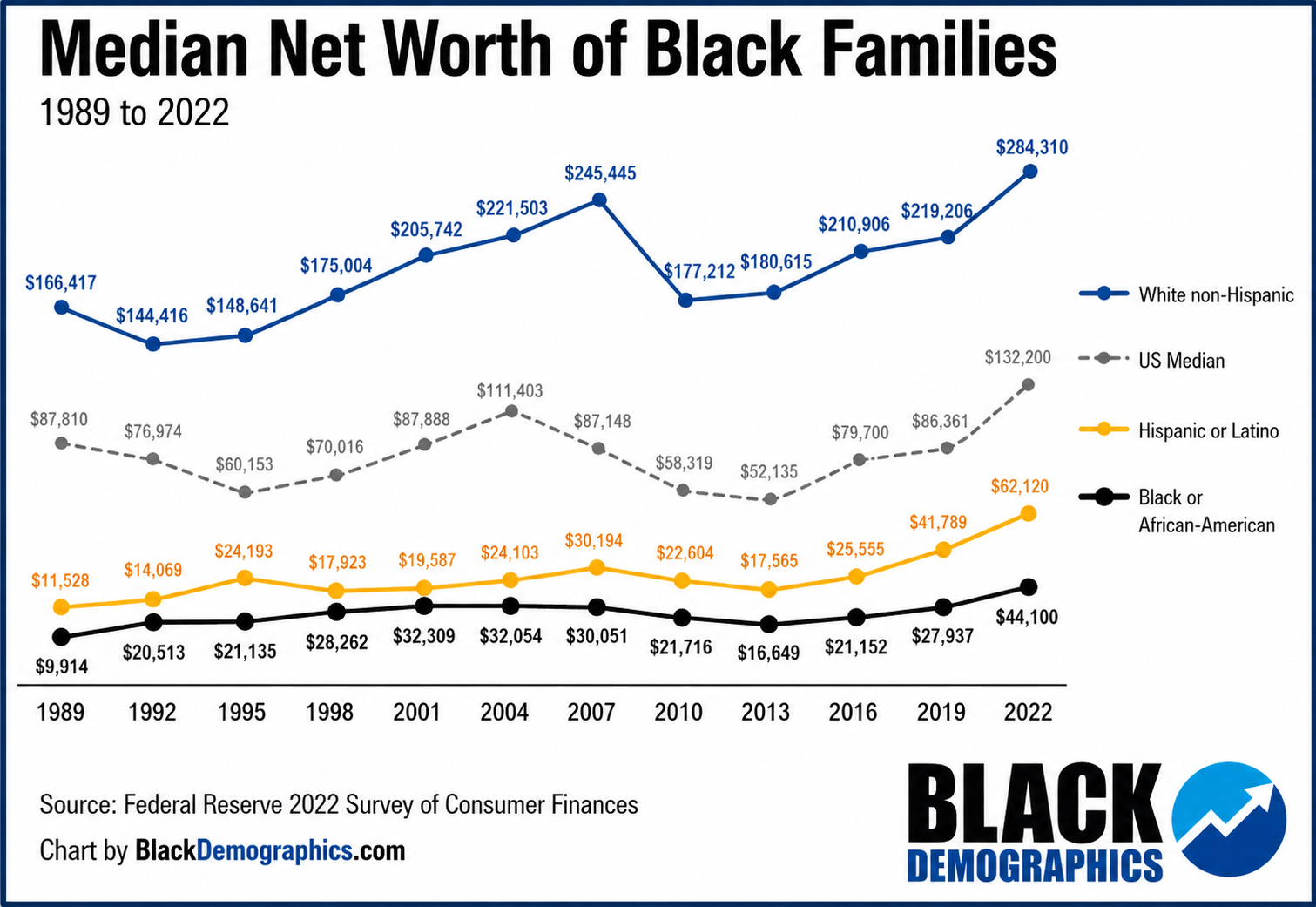

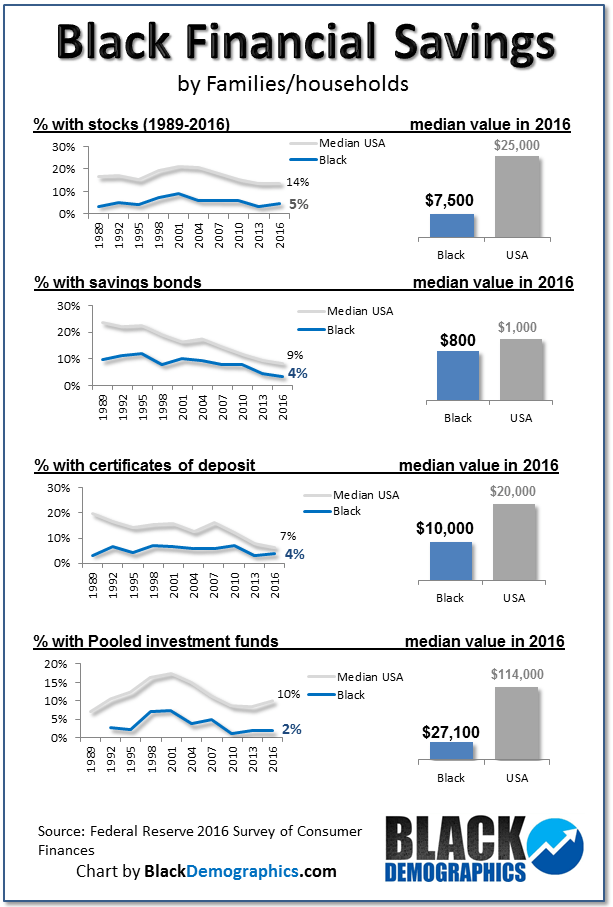

One way of measuring wealth, in addition to income, is by looking at “net worth.” Net worth is calculated by taking a household’s assets and subtracting its liabilities. Assets may include things like real estate, stocks, interest-earning accounts, business equity, vehicles, and more.

In 1989, the median net worth of Black families was $9,914, which was far lower than White families, who had a median net worth of $166,417. By 2001, the median net worth for African American families rose to $32,309, while the White median net worth continued to grow, reaching $245,445 by 2004.

However, due to the “Great Recession,” the median net worth of Black families dropped to $16,469 by 2013. This was lower than it had been in 1992 and lower than at any point since then. The median net worth for White families also declined, but only to $177,212, making the Black-White wealth gap even wider than it was in the 1980s or 1990s. As the economy improved, wealth increased, but much more slowly for Black households than for all American households. By 2022, the Black-White wealth gap had grown wider again than at any point in the last 30 years.

History of the Black Middle Class

There has been a Black middle class in America since before emancipation from slavery. However, during that time, it was affected by an extreme form of colorism that carried over from slavery. This was partly because many fair-skinned Black slaves were often favored and given indoor work, as they were seen as less threatening. In some cases, they were also fathered by slave owners.

Despite this, they were still segregated from Whites after slavery. At the same time, they were often isolated from, and sometimes even scorned by, the rest of the Black community. Many developed their own institutions, businesses, and places of worship. Some Black colleges even asked for photos with applications to limit the number of dark-skinned students they admitted.

Most of those who considered themselves middle class were still redlined into inner cities and lived among working-class and poor Black communities. Things began to change with the Civil Rights Movement. Since the 1960s, the Black middle class has grown significantly. African Americans have moved into more white-collar jobs and are more educated than ever before. No longer isolated or identified mainly by skin tone, many integrated into White middle-class neighborhoods, while others developed their own Black middle-class communities.

By the 1990s, middle-class Black American communities had become well established and were no longer closely tied to lower-income Black populations. Communities such as South DeKalb (Atlanta), Prince George’s County (DC/MD), and Baldwin Hills (Los Angeles) developed across the country and continue to grow today.

Assets

Affects of Wealth During the Great Recession

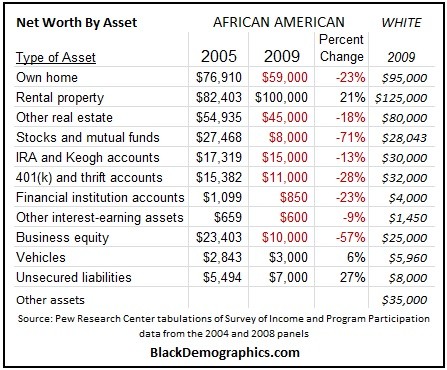

According the Pew Research Center Black household net worth is concentrated more in home ownership rather than other assets. Since African American home ownership and value was hit hardest in the recession by -23% and the majority of wealth was in their homes they lost much of their net worth. Blacks also lost larger percentages in stocks and mutual funds (-71%), 401K (-28%), and Business equity (-57%).